Understanding Your Credit Score: Components, Maintenance, and Impact

Key Points:

A credit score is an extremely important part of your financial life. It can impact the rate you pay on loans and sometimes whether you can even obtain a loan.

Credit scores or FICO scores are calculated based on several components of one’s credit history and makeup; these components have various levels of importance.

We believe that the keys to achieving and maintaining a high credit score are to understand how it is calculated, how to increase it, and how to monitor it.

As financial advisors, we often get inquiries from clients about why they didn’t receive the lowest mortgage rate despite having ample income and assets. The underlying issue may contain a number of factors but in most cases, it has to do with the client’s credit score. A credit score is an extremely important part of our financial lives. It shows potential lenders that you are a financially responsible individual and that there are minimal risks in lending money to you. Although many people may realize the importance of a high credit score, they may not understand what makes up a credit score or how they can increase and monitor it.

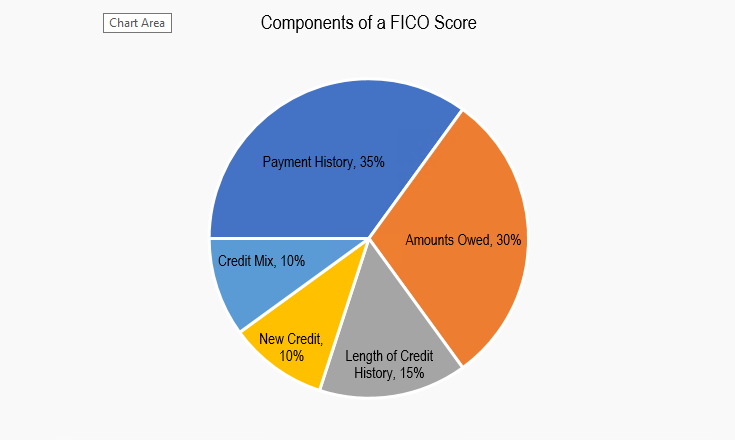

Credit scores, commonly known as FICO credit scores, were developed in the late 50’s by the Fair Isaac Corporation (FICO) to enable U.S. financial lending institutions to make consumer credit decisions. According to myFICO, the consumer division of FICO, scores are calculated based on five major components: payment history, amounts owed, length of credit history, amount of new credit, and credit mix.¹ (See Figure 1.)

FICO_Score_PieChart1_Updated2

Figure 1. Source: myFICO, www.myfico.com

Payment History: This represents the largest portion of the total credit score. Lenders are concerned with whether you are making payments and whether those payments are on time. They also place a heavier emphasis on repayment of past debt. Generally, defaulting on an installment-type of loan, such as a mortgage, would have a more significant impact on your credit score than defaulting on a credit card or a utility bill.

Amounts Owed (or Credit Utilization): This is the second largest portion of the total credit score. In essence, credit utilization is the part of the calculation that looks at how much of your available credit you are using. Borrowers that consistently max out their credit cards send signals to lenders that they are incapable of handling debt responsibly.

Length of Credit History: This is based on the length of time each of your credit accounts have been opened and the length of time since each account has had activity. Generally, the longer and more active your credit history is the better your credit score will be.

New Credit: This portion of the credit score calculation looks at how recently you have applied for new credit. Opening numerous credit accounts in a short period of time tells lenders that you may have a liquidity issue.

Credit Mix in Use:This part of the calculation looks at the total mix of all your credit accounts. Making timely payments on numerous types of credit accounts (e.g., credit cards, auto loans, mortgages, etc.) let’s lenders know that you can handle debt responsibly.

One of the most effective ways to increase your credit score is to pay your credit accounts on a consistent and timely basis. Couple this with not fully utilizing your available credit and, theoretically, you will be 65% of the way towards a good credit score. One thing to keep in mind regarding credit utilization is that having a single credit card causes the calculation to be based entirely on the available credit from that one account. Therefore, contrary to common belief, having one credit card, using it for everything, then paying off the full balance every month may actually hurt your credit score more than it helps.

To stay on top of your credit and avoid surprises, it is important to monitor your credit score at least once a year. One of the easiest ways to do this is to check your credit reports. There may be incorrect information from improper coding or fraudulent activity that is factored into your credit score. If you find errors in your report, you can dispute the inaccuracies with the Consumer Financial Protection Bureau.

There are three main ways to get a full credit report for free. It can be obtained through a personal finance website, a non-profit counselor, or a consumer credit reporting bureau. Free personal finance websites (like Credit Karma or Free Credit Score) offer access throughout the year to one or two reports that are updated periodically. If you are a potential borrower, non-profit credit counselors and HUD-approved housing counselors can provide you with a free credit report as well. Lastly, you can obtain a credit report from one of the three major credit reporting bureaus: Equifax, Experian, or TransUnion. Federal law allows you to get a free copy of your full credit report every twelve months from any of these three companies.

Many credit card companies such as Discover or American Express now provide monthly statements that include your FICO score from one of the credit bureaus. You can also see your score intra-month by logging into your credit card’s online account. Credit card companies will provide a free "credit report summary," but typically this report is incomplete. Although logging into one of these credit card providers is a good way to do a quick check on your score, we recommend obtaining your full report to get all of the details.

Understanding and knowing your credit score can mean the difference between qualifying for a loan and getting declined, or getting the best interest rate on a loan. Familiarizing yourself with the way that the FICO score is calculated will help you understand how to increase your credit score, positioning yourself for high quality loans. Remember that obtaining your credit score report is easy and, most of the time, free. Should you require assistance or have any questions as to how you can improve your credit situation, feel free to contact Capstone and one of our Certified Financial Planner™(CFP®) professionals can assist you.

Sources ¹http://www.myfico.com/credit-education/whats-in-your-credit-score