Bonds are down – Should you make any changes to your portfolio?

KEY POINTS

Stocks and bonds broadly declined worldwide in the first quarter of 2022. We remain optimistic on the stock market amid a still supportive fundamental backdrop that is likely to continue for some time. We also remain optimistic on the bond market (with higher yields) despite its recent uncharacteristically high volatility.

In the first quarter, the U.S. economy remained on solid footing while most major economies abroad withstood the initial impact of the war. Looking ahead, the U.S. economy is likely to go through a modest growth slowdown, while Europe likely enters a recession and China’s growth slows further.

In the first quarter, bonds markets in aggregate experienced one of their worst three-month declines in decades. We answer the question of whether investors should consider making any changes to their portfolio.

Global investors face a challenging market environment, with expectations of higher inflation, tighter monetary policy, and the impacts of the Russia-Ukraine war. We outline ways that investors should position portfolios for above-trend inflation and rising interest rates over the next few years.

MARKET REVIEW

STOCKS DECLINED IN THE FIRST QUARTER AMID MONETARY POLICY AND GEOPOLITICAL UNCERTAINTY

After an exceptionally calm 2021, we’ve seen a return to a more normal (higher) level of volatility in stock markets so far in 2022. A meaningful upward change in interest rate policy expectations triggered sharp selloffs, particularly in highly-valued growth sectors. Russia’s invasion of Ukraine further amplified market volatility globally. At one point, stocks broadly entered correction territory, down over 10%, with some parts of the market down over 20%. Despite recovering somewhat in March, stocks in aggregate finished the quarter in the red.

BOND PRICES FELL AMID A SHARP RISE IN INTEREST RATE EXPECTATIONS

Bonds sustained their worst quarterly decline in decades as the markets reset expectations for how quickly the Federal Reserve and other central banks will raise interest rates. Rate policy timetables accelerated due to inflation remaining elevated longer than most expected, a dynamic worsened by the spike in oil prices after Russia invaded Ukraine. The result is that yields - which move in the opposite direction of bond prices- have risen at their fastest pace in years.

MARKET OUTLOOK

HEALTH OF THE ECONOMY AND LEVEL OF INTEREST RATES ARE STILL FAVORABLE FOR STOCK MARKET RETURNS

We remain optimistic on the stock market amid a still supportive fundamental backdrop that is likely to continue for some time. At the forefront of this outlook is long-term corporate earnings growth, which should continue to be positive, albeit at a slower pace. Higher interest and inflation rates will affect market constituents differently, with growth-oriented, less profitable companies negatively impacted and value-oriented, more profitable companies positively (or less) impacted. Regardless of higher inflation and interest rates, the economy thus far remains healthy, and financial conditions (i.e., interest rate levels) are still favorable enough to support stock market returns.

RECENT STOCK MARKET VOLATILITY IS LIKELY TO REMAIN THROUGHOUT 2022

Although stock market volatility subsided over the last few weeks of the first quarter, we expect market swings (both up and down) to increase again. Plenty of factors will likely contribute to increased volatility throughout 2022, including uncertainties about the Russia-Ukraine war, central bank rate decisions, company earnings, and looming electoral events. Additionally, there is still the potential virus risk and the impact it could have (albeit smaller) on the still-ongoing global recovery. We continue to believe that the more speculative, expensive, and higher-risk areas of the market are likely to be particularly vulnerable in this environment.

MOST OF THE BOND MARKET DECLINES ARE LIKELY BEHIND US FOR THIS CURRENT RATE HIKING CYCLE

We also remain optimistic on the bond market despite the uncharacteristically high volatility we experienced with bonds in the first quarter. Although bonds returns are down materially so far this year, the result is that current bond yields are now significantly higher, which will increase returns going forward. Moreover, investors should not extrapolate that the bond losses experienced in the first quarter will continue throughout the remainder of the year. Notwithstanding another unexpected inflation shock (or growth shock), we believe that most of the bond market declines are likely behind us for this current rate hiking cycle.

POLICY RATES ARE TO INCREASE AT A FASTER PACE, BUT THIS IS BROADLY EXPECTED NOW

The Federal Reserve will increase short-term policy rates at a faster pace than what was expected late last year and early this year. A big part of the reason for faster rate increases is that it is now evident that the peak in inflation is likely to be higher and take longer to reach than economists previously estimated. The change in pace for rate hikes has partly to do with the lingering pandemic supply constraints and surging demand. The change is also partly because of the unexpected war and impact of such on energy and food costs.

However, faster rate increases do not mean it’s a foregone conclusion that bonds will lose money going forward amid the rate hikes. The reality is that markets already have likely factored most, if not all, of these new expectations into bond prices.

ECONOMIC REVEW

RUSSIA-UKRAINE WAR INJECTED SIGNIFICANT UNCERTAINTY INTO THE GLOBAL ECONOMY

Prior to the Russian invasion of Ukraine, economic signals were encouraging through February as the Omicron wave retreated and supply chains began to improve. In March, already elevated raw material costs were boosted by a barrage of sanctions that impacted commodities and energy markets and further constrained supply chains. Higher oil prices stemming from Russia's invasion of Ukraine have increased inflation risk and downside growth risk.

U.S. ECONOMY REMAINED ON SOLID FOOTING

Economic data in the U.S. have increasingly indicated stickier inflation and an increasingly tighter labor market. (See Figure 3.) This data drove the Federal Reserve to raise the federal-funds rate by 0.25 percentage points in March for the first time since December 2018. The Fed also communicated more aggressive forward guidance around future rate hikes. So far this year, the impact of rising prices and interest rates in the U.S. has not yet negatively affected consumer spending to a large degree.

INTERNATIONAL ECONOMY WITHSTOOD THE INITIAL IMPACT OF THE WAR

Internationally, the relaxation of pandemic restrictions generally helped business activity weather the initial shock from the Russia-Ukraine war. Eurozone and UK economic indicators were surprisingly resilient throughout the first quarter, with manufacturing and service sector growth still gaining momentum despite hot inflation and direct geographic and economic ties to the conflict. China also released stronger-than-expected economic data throughout much of the first quarter. However, China’s economy has been stabilizing at a lower growth rate, and significant headwinds developed in mid-March as the increase in COVID-19 cases led to renewed restrictions and shutdowns.

ECONOMIC OUTLOOK

THE U.S. ECONOMY IS LIKELY TO GO THROUGH A MODEST GROWTH SLOWDOWN

The U.S. economy will continue to grow, but the impacts of higher inflation and interest rates will likely result in a modest growth slowdown. The U.S. has a relatively diversified and services-heavy economy and is mostly energy independent. As a result, the U.S. is less sensitive to energy price shocks and should be able to avoid a recession. Furthermore, higher interest rates will negatively impact certain areas of the economy (housing, for example). However, interest rates will still be relatively low, and the impact of higher rates will take some time to sink in. Although the Fed is currently focused on bringing down high inflation by slowing the economy, it will aim to do so without tipping the economy into a recession.

EUROPE IS LIKELY TO ENTER A RECESSION WHILE CHINA’S GROWTH SLOWS FURTHER

Growth and inflation in Europe are more vulnerable to the energy price shock, as economies across the region are manufacturing and trade-heavy relative to the US. Energy price impacts are likely to be peculiarly acute in the Euro Area, which imports a significant amount of its natural gas and crude oil from Russia. As such, a wartime recession in Europe is likely if the war in Ukraine drags on, and the rise in producer prices is eventually passed through to consumers. The severity of a recession could be mitigated if European countries move forward with fiscal measures to offset rising costs.

China’s economy could suffer in the short term if governments continue to impose COVID-19 lockdowns. Additionally, China’s close trading relationship with the European Union could also expose it to a recession in Europe. Should China’s growth slow enough, the Chinese central bank will probably cut interest rates soon, while most other central banks worldwide are moving in the opposite direction.

THE GLOBAL ECONOMY WILL LIKELY EXPERIENCE A MORE EXTENDED PERIOD OF HIGH INFLATION

Inflation is still expected to peak and then moderate gradually this year, though we’re now unlikely to see the peak for a few more months because of the Russia-Ukraine conflict. A protracted period of high food and energy prices will likely hurt consumer demand for goods and services that are either discretionary or able to be substituted by something cheaper. However, growth should remain supported by continued post-pandemic economic reopening, low unemployment, and a strong consumer financial position.

ON THE MINDS OF INVESTORS

BONDS ARE DOWN– SHOULD YOU MAKE ANY CHANGES YOUR PORTFOLIO?

In the first quarter, bonds markets in aggregate experienced one of their worst three-month declines in decades. Forecasts have been predicting that bond prices would fall and yields (interest rates) would rise over several years, although no one anticipated a shift as abrupt as this one. While any negative performance can be difficult, negative bond returns can feel particularly shocking. However, declines within the bond market are not unprecedented. (See Figure 4.)

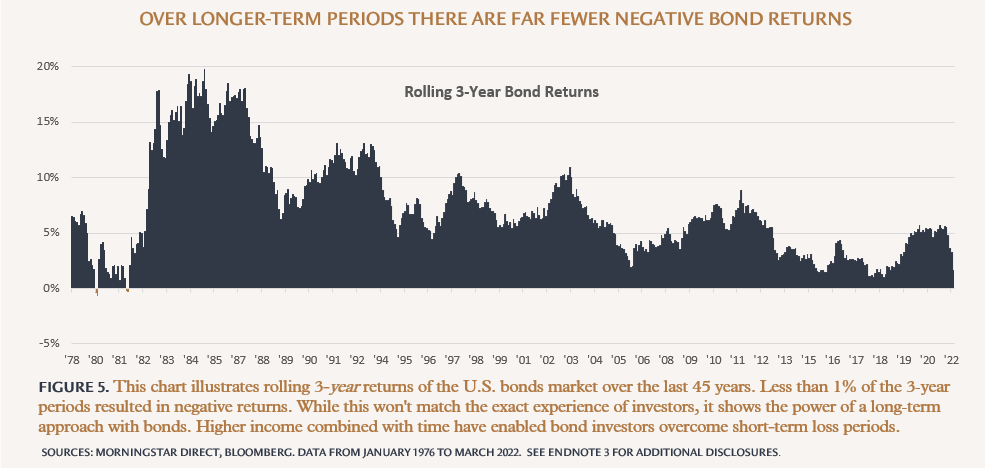

Investors typically think of bonds as investments that will never have negative performance, but that is not the case. Investors must take on marginal risk to enjoy the potential rewards of investing in bonds (i.e., providing defensiveness in a portfolio while earning a reliable income return). The good news is that disciplined investors with a longer-term approach have historically experienced far fewer negative periods with bonds. (See Figure 5.) The reason for this is that the vast majority of a bond return comes from the income (yield), which goes up whenever bonds experience price declines; higher yields mean more income, which over time, makes up for drops in price

TUNE OUT THE NOISE

With Fed officials signaling a more hawkish policy stance, some investors might choose to sit out for some time by switching to cash or shorter‐duration bonds. However, the timing and direction of changes to the Federal Funds rate, let alone the 10-year U.S. Treasury rate, are difficult to predict and don’t indicate how other interest rates and investors will react. Even if it may appear obvious, no one can predict what will happen moving forward, but having a plan you can stick with may help during short‐term periods of volatility.

MANAGE TAX LIABILITIES THROUGH LOSS HARVESTING OPPORTUNITIES

Tax loss harvesting, which we implement in client portfolios, is a potential action item to take during material bond market downturns. When appropriate, investors may choose to sell to realize capital losses, which they may use to offset current or expected future capital gains or income. To continue earning income, investors can reinvest the proceeds from the sale in a different bond investment.

REBALANCING AND REINVESTING

Rising interest rates provide the opportunity to purchase bonds that are paying higher yields which means more income. When interest rates rise, rebalancing (into bonds from stocks) and ongoing reinvestment (of interest and principal back into bonds) enable buying bonds at lower prices (hence higher yields). This systematic approach, which we implement in client portfolios, will help to increase the income yield component of future total returns for bonds portfolios. Over time, the higher yields on reinvested cash flows outweigh the short-term market declines.

PORTFOLIO MANAGEMENT

STAYING INVESTED AND DISCIPLINED

Global investors face a challenging market environment, with expectations of higher inflation, tighter monetary policy, and the impacts of the Russia-Ukraine war.

This year has been particularly difficult because prices of both stocks and bonds broadly have fallen, leaving most investors in negative territory through the first quarter, regardless of their asset allocation. However, it is tough times like this when investors must maintain a long-term perspective and stick to their investment plan even though they don’t see any recent portfolio gains.

Even during short-term periods like this, when diversification isn’t working as well as it usually does, there are still opportunities to improve long-term investment outcomes, which we’ve been taking advantage of for clients.

Given that most asset classes are down year-to-date, there haven’t been many chances to rebalance portfolios recently. However, the declines across asset classes had presented opportunities for us to tax loss harvest bond investments, as noted earlier, and stock investments around when stock markets were trading near their lows for the year. As a result, we successfully achieved future tax benefits for clients while keeping portfolios fully invested.

Additionally, recent market declines have resulted in material valuation improvements across asset classes relative to the start of the year. As a result, this has allowed investors to enter the market at a relative discount. As such, for portfolios sitting on material cash balances, we have been taking the opportunity to accelerate dollar-cost average investment plans into all asset classes

MAINTAINING GLOBAL DIVERSIFICATION

Investors that have globally diversified portfolios inevitably face periods of geopolitical risk. Sometimes these events lead to restrictions, sanctions, trade tariffs, and other market disruptions. No one can predict what type of events will happen, when they will occur, or how long they will last. However, we can plan for them by appropriately diversifying portfolios and limiting exposure to higher-risk areas of the market.

Direct exposure to Russia and Ukraine in Capstone portfolios was minimal, measured in basis points. The limited exposure was held in our recommended international stock and bond fund strategies; however, it was not material prior to the invasion of Ukraine and is essentially zero currently. This unfortunate situation is a prime example of why we believe that broad diversification is the most effective way to mitigate the risk of unexpected events. Of course, this philosophy applies to other crises, like natural disasters, social unrest, and pandemics.

TILTING TOWARD VALUE-ORIENTED STOCKS

Higher interest rates have brought volatility to the markets, particularly to stock market segments that previously benefited from near-zero interest rates, like large-capitalization and growth-oriented companies with low profit margins. As a result, many of these stocks reached valuations not justified by their fundamentals and now face headwinds resulting in material underperformance so far this year relative to smaller-cap, value-oriented, and more profitable companies.

Capstone stock portfolios continue to tilt toward relatively more profitable, less expensive, and smaller-cap stocks. We expect these types of stocks to continue providing strong relative performance over the next few years as the global recovery continues and interest rates climb higher. While we continue to overweight these stocks, we still maintain some exposure to larger-cap stocks and growth sectors for diversification purposes.

HEDGING AGAINST INFLATION

Given current and likely prolonged inflation risk, we will continue to keep cash levels down to a minimum in portfolios and recommend that clients maintain low cash levels in outside accounts.

Stock allocations are already set up to do relatively well in an increasingly high inflation environment. Capstone stock portfolios include diversified allocations across various sectors, including energy, materials, and utilities. These sectors tend to do particularly well in an above-trend inflationary environment because of their ability to pass on price increases to consumers and businesses.

Additionally, we will continue to allocate toward “real assets” like real estate and infrastructure equities, which tend to provide increased inflation protection to portfolios via rising rents and contracted cash flows that are often automatically adjusted with inflation. In addition, we expect real estate and infrastructure to continue their strong performance with the ongoing resumption of global economic activity and significant investment in (and high demand for) these assets.

Given what is likely to be a high-inflation regime for some time, we are exploring opportunities to potentially add more inflation hedging portfolio components.

SOURCES & ENDNOTES

¹ U.S. stock returns are represented by the Russell 3000 Index. International stock returns are represented by the MSCI ACWI Ex USA IMI. U.S. bond returns are represented by the Bloomberg Aggregate Bond Index. International bond returns are represented by the Bloomberg Global Aggregate Ex USA Hedged Index.

² Stock returns are represented by the S&P 500 Index Total Return. Bond returns are represented by the Bloomberg Aggregate Bond Index Total Return.

³ Bond returns are represented by the Bloomberg Aggregate U.S. Bond Index (Total Return). 3-month returns are cumulative. 3-year returns are annualized.

Past performance does not guarantee future results. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

IMPORTANT DISCLOSURE INFORMATION

Please remember that different types of investments involve varying degrees of risk, including the loss of money invested. Past performance may not be indicative of future results. Therefore, it should not be assumed that future performance of any specific investment or investment strategy, including the investments or investment strategies recommended or undertaken by Capstone Financial Advisors, Inc. (“Capstone”) will be profitable. Definitions of any indices listed herein are available upon request. Please contact Capstone if there are any changes in your personal or financial situation or investment objectives for the purpose of reviewing our previous recommendations and services, or if you wish to impose, add, or modify any reasonable restrictions to our investment management services. This article is not a substitute for personalized advice from Capstone and nothing contained in this presentation is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Investment decisions should always be based on the investor’s specific financial needs, objectives, goals, time horizon, and risk tolerance. This article is current only as of the date on which it was sent. The statements and opinions expressed are, however, subject to change without notice based on market and other conditions and may differ from opinions expressed by other businesses and activities of Capstone. Descriptions of Capstone’s process and strategies are based on general practice, and we may make exceptions in specific cases. A copy of our current written disclosure statement discussing our advisory services and fees is available for your review upon request.