Investment Perspective Q4 2018: How might the midterm elections affect the markets?

Key Points:

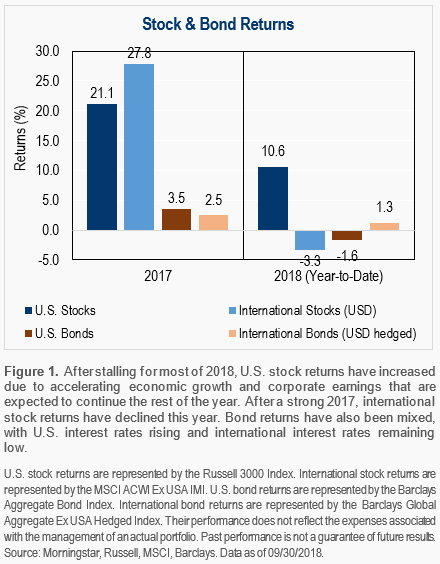

Strong corporate earnings growth has helped push the U.S. stock market to all-time highs, while international stocks have struggled due to a host of reasons. Bond returns have also been mixed, with U.S. interest rates rising and foreign interest rates remaining low. Returns for U.S. bonds and international stocks are likely to be better going forward.

The U.S. economy continues running at a faster pace without a significant increase in inflation. Meanwhile, international economic growth broadly remains positive; Europe and emerging markets, however, have recently experienced setbacks. Aggregate global economic growth for the U.S. and international economies is expected to stay on pace with last year’s 3.7%¹ growth rate.

The upcoming U.S. midterm elections in November are going to be a center of focus for their potential impact on U.S. policy, the economy, and corporate earnings. Market volatility is expected to increase leading up to the contests, but it will likely be short-lived regardless of the results.

Strong Growth and Earnings Push U.S. Stocks Higher

The U.S. stock market has started to recover from the inflation- and trade-fueled risk that put last year’s strong rally on hold for most of 2018. A strengthening economy and double-digit corporate earnings growth have been keys to pushing the U.S. stock market to all-time highs. For International stocks, the story has been different especially in emerging markets, where trade tensions, currency moves, and political and economic disruptions have offset otherwise solid fundamentals. Many countries abroad are in early stages of economic and earnings recoveries, and are still on track to improve despite recently negative international stock returns.

Relative to stocks, the story with bonds in 2018 is flipped, with U.S. bonds down and international bonds up. (See Figure 1.) Firming inflation and accelerating economic growth in the U.S. prompted the Federal Reserve (the Fed) to raise interest rates three times so far this year, which has put downward pressure on U.S. bond returns. Since the U.S. economy is growing faster than expected, the latest message from the Fed is that it intends to maintain its gradual pace of interest-rate increases into 2019. In contrast, most major international central banks have kept interest rates anchored at low levels to support their economies.

Bonds and International Stocks Poised to Do Better

With U.S. corporations expected to report double-digit earnings growth for the third and fourth quarters, U.S. stocks are likely to continue moving higher, but not without bumps along the way from new developments on trade policy, interest rates, and the outcomes of the U.S. midterm elections. Earnings growth will also likely continue for international companies given the overall strength of the global economy. While challenges certainly remain abroad, we think international stock returns will likely pick up steam again, especially given their relative cheapness. Additionally, U.S. bond returns are likely to improve because today’s higher interest rates should give a boost to bond returns going forward.

The U.S. Economy Continues Running at a Fast Pace

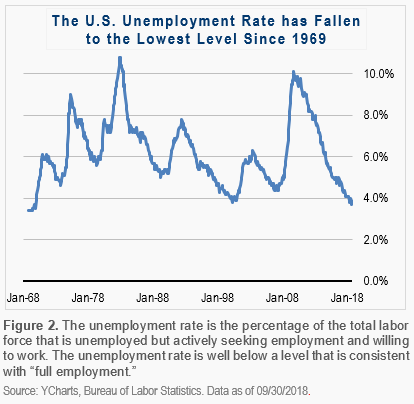

The U.S. growth spurt that started in the second quarter carried over into the third quarter. Strong consumer, business, and government spending have accelerated the U.S. economy. While the recent tax cuts have helped spur some of this spending, a healthy job market has given consumers the confidence to spend. The U.S. unemployment rate has fallen to the lowest level since 1969 on the back of very healthy business conditions. (See Figure 2.) Additionally, the strengthening of the economy has happened without a significant increase in inflation, allowing the Fed to take its time raising interest rates and not disrupt growth.

Europe and Emerging Markets Have Slowed Down

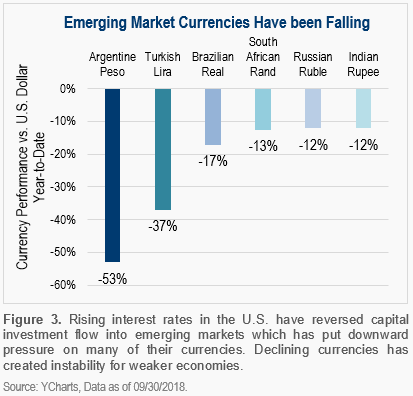

Outside of the U.S., economic growth broadly remains positive. However, Europe and emerging markets have recently experienced setbacks. In Europe, the 19-country eurozone still struggles with political fragility and immigration tensions while the UK remains hindered by the impacts of “Brexit.” Meanwhile, several emerging market countries have faced instability over the past six months from a sharply rising U.S. dollar. As the dollar has risen, currencies in emerging markets have fallen (see Figure 3), which as a result, have raised the price of their imports, made it harder for them to manage dollar-denominated debts, and forced their central banks to raise interest rates quickly.

Global Economic Growth Will Likely Remain on Track

Aggregate global economic growth for the U.S. and international economies is expected to stay on pace with last year’s 3.7%1 growth rate. Unfortunately, according to the latest forecasts from the International Monetary Fund (IMF), global growth is not likely to have accelerated this year relative to last year. The IMF has also said that the recently enacted tariffs between the U.S. and China have slowed global trade volume. Trade tensions together with the recent turmoil in emerging markets have substantially offset the recent U.S. growth spurt. The good news going forward is that central banks broadly remain patient and accommodative.

Midterm Elections Are Likely to Cause Volatility

The upcoming U.S. midterm elections in November are going to be a center of focus for their potential impact on U.S. policy, the economy, and corporate earnings. The uncertainty that comes with political events typically causes market volatility—leading up to and sometime after the event—and we don’t expect this election to be any different. This time around, investors will be concerned about how the outcome of the midterm elections might impact everything from trade, tax policy to potential impeachment proceedings.

The key outcome of this election will be whether Republicans maintain control of both chambers of Congress, as the result could influence the economy and financial markets. (See Figure 4.) If Republicans retain the majority in both the House and the Senate, many expect a continuation of the current administration’s policies (i.e., tax cuts, government spending, deregulation) and minimal market impact. If, on the other hand, the House, the Senate, or both flip to the Democrats, there could be an abrupt shift in policy that would likely take markets by surprise. Though, even in that situation, history shows that market volatility caused by elections is usually short-lived. We would expect that to be the case this time as well.

Regardless of the outcome, current economic fundamentals will likely remain in place after the election. Unfortunately, improvements with tariffs and trade tensions are not expected because decisions on these policies reside largely in the executive branch. Uncertainty about trade wars and other political rhetoric would likely continue to shake markets.

Portfolio Management

Why Now is Still a Good Time to Invest

With the U.S. stock market reaching “all-time highs,” many are curious as to whether now is a good time to invest; a common concern is that the market “can only go down from here.” While stock markets have always gone down after reaching high points, they have also always recovered and moved even higher afterward. History shows that stock markets have regularly reached new all-time highs, and today, there is nothing that suggests this trend will not continue in the years ahead.

One of the principals of our philosophy is that most investors should invest as much as they can for as long as possible; this can be the most effective way to grow wealth over time. Our philosophy is contrary to an approach that suggests that one should try to “time the market”: get out when markets reach all-time highs and buy back in later, or merely wait to invest new money until the next time the market goes down. Although this approach sounds logical, in practice, it is tough to get right more times than not and can often result in missing out on significant returns. Market timing is not an enduring investment strategy.

Another thing to consider is that today, there is only one major market at all-time highs: the U.S. stock market. In other words, there are other markets and asset classes, like international stocks, real estate, and bonds, that are not at all-time highs. The various markets available for us to invest in today are almost always at different points relative to each other, and do not typically move (up and down) in sync. When it comes to investing, diversifying a portfolio across many markets ensures that it is positioned to capture returns wherever they occur and of course, to alleviate the short-term pain of a market coming down from another all-time high.

Sources

¹The International Monetary Fund, World Economic Outlook, October 2018

Important Disclosure Information

Please remember that different types of investments involve varying degrees of risk, including the loss of money invested. Past performance may not be indicative of future results. Therefore, it should not be assumed that future performance of any specific investment or investment strategy, including the investments or investment strategies recommended or undertaken by Capstone Financial Advisors, Inc. (“Capstone”) will be profitable. Definitions of any indices listed herein are available upon request. Please contact Capstone if there are any changes in your personal or financial situation or investment objectives for the purpose of reviewing our previous recommendations and services, or if you wish to impose, add, or modify any reasonable restrictions to our investment management services. This article is not a substitute for personalized advice from Capstone and nothing contained in this presentation is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Investment decisions should always be based on the investor’s specific financial needs, objectives, goals, time horizon, and risk tolerance. This article is current only as of the date on which it was sent. The statements and opinions expressed are, however, subject to change without notice based on market and other conditions and may differ from opinions expressed by other businesses and activities of Capstone. Descriptions of Capstone’s process and strategies are based on general practice, and we may make exceptions in specific cases. A copy of our current written disclosure statement discussing our advisory services and fees is available for your review upon request.