Investment Perspective Q2 2018: Is a trade war likely to happen?

Key Points:

Stocks fell in the first quarter on concerns of rising interest rates and escalating trade tensions. Higher rates also resulted in modest declines for U.S. bonds; in contrast, international bonds were the only major asset class to deliver positive returns. We expect stocks to recover quickly, even if they were to drop significantly more, and bond returns to be challenged but positive.

The acceleration in the U.S. economy that started at the end of last year has extended into 2018. Meanwhile, economic recoveries continued across Europe and Asia but are not yet at full steam. We still expect global economic growth to continue and moderately accelerate throughout the year with minimal direct economic impact from the proposed tariffs. We don’t think a trade war is likely.

Global and sector diversification has helped mitigate losses so far this year, particularly within bonds, real estate, and infrastructure stocks. Considering our outlook that markets are inevitably going to recover given solid fundamentals, we think that times like this provide long-term investors the opportunity to invest cash and rebalance their portfolios.

Modest Market Declines Didn’t Feel That Way

Following one of the best years for global stock returns, markets took a breather in the first quarter of 2018. (See Figure 1.) The January through March decline marked the first quarterly loss for global stocks since the third quarter of 2015. While the fall in stocks was modest, it didn’t feel that way with the return of wild market swings (i.e., six trading days of +/- 2%) and stocks ending the quarter down 7% from their late-January highs. Turbulence returned to the markets over concerns of rising interest rates and escalating trade tensions. However, we think this is a return to a more normal level of market volatility rather than a harbinger of bad things to come.

While most of the attention was on stocks, higher interest rates in the U.S. also resulted in modest declines for U.S. bonds. In contrast, international bonds were the only major asset class to deliver positive returns in the first quarter. Because most major foreign country economies are not currently growing as fast as the U.S., their interest rates have either held steady or declined. Despite faster U.S. growth, we don’t think the recent jump in U.S. rates is indicative of a sharp move higher; instead, it will likely be a more gradual path that will be more favorable for bonds.

Stocks Could Fall Further But Should Recover Quickly

Current policy and geopolitical-related issues are likely to continue driving big market swings going forward. However, the fundamental backdrop for stocks remains strong. With continued corporate earnings growth and the passage of both U.S. tax cuts and a government spending package, stocks are likely to recover quickly, even if they were to drop significantly more. We still expect positive returns from stocks, though they are likely to be lower than recent years. Bonds, on the other hand, are likely to continue to be challenged. Although, if the gradual interest rate rise scenario plays out, bond returns will likely remain positive with higher interest income offsetting the effects of declining values.

U.S. Economy is Accelerating, But Not Overheating

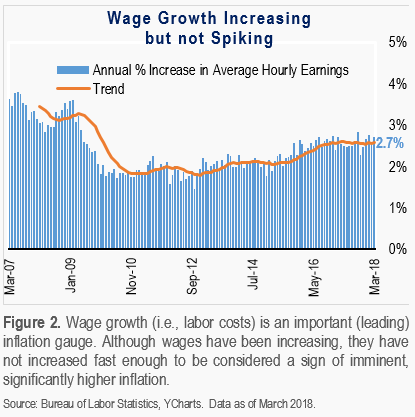

Despite stock markets indicating otherwise, bond markets have confirmed that U.S. economic growth has accelerated. Growth averaged 3% in the final three quarters of 2017 and the momentum has extended into 2018, confirmed by the Federal Reserve (the Fed) hiking rates again and raising its growth forecasts. Recent labor market reports have continued to show strong job creation and higher wage growth. While wage growth has been a market concern as it could spark overall inflation, we think this concern is a little overblown at this time given the gradualness and current level (2.7%) of wage increases. (See Figure 2.)

Economies Abroad Improving But Still Need a Boost

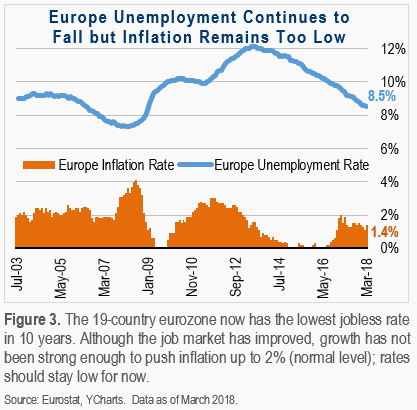

Outside of the U.S., economic recoveries continued across Europe and Asia. However, a common theme occurring in major countries is that their economies are growing, though not fast enough. For example, in the 19-country eurozone (the 2nd largest economy in the world¹), unemployment has dropped to its lowest level (8.5%) since December 2008. (See Figure 3.) But while the number of people out of work has fallen, inflation remains very low (1.4%), an indication that there is still “slack” in the economy. So, unlike in the U.S., the European Central Bank remains committed to keeping interest rates low until the economy is on firmer footing.

Global Growth Will Likely Remain on Track

We still expect global economic growth (U.S. and abroad) to continue and moderately accelerate throughout the year. Despite recent headlines about tariffs and the resulting market reactions, almost all the various economic indicators we monitor are still trending in a positive direction, and there are no imminent signs of a global recession. While major international countries are struggling to get to “full capacity” growth, central banks remain patient and accommodative. With the U.S. economy further along, the recently passed tax cuts and government spending plans should help to offset the Fed increasing rates.

Impact of Tariffs and Likelihood of Trade Wars

Although there has been a lot of apprehension about recently proposed tariffs, we expect minimal direct economic impact given how much the targeted goods represent as a percentage of total U.S. imports. The Trump Administration recently announced its imposition of steel and aluminum tariffs followed by a proposed package of tariffs and trade penalties on approximately $50 to $150 billion of goods from China. In total (steel, aluminum and $50-$150B China goods) represent only about 4% to 7% of U.S. imports, a small fraction of trade between the U.S. and other countries. (See Figure 4.) Scale aside, the benefit of a tariff (enhanced industry competition) is usually short-lived because it is typically offset by retaliatory tariffs.

Given the potential risk of disrupting the economy, we believe that there is a low likelihood that the current administration will significantly alter U.S. trade policy. Financial markets serve as a leading indicator for the economy, and the negative reaction to headlines of tariff talk and posturing validate the serious consequences of a full-blown trade war and its damaging economic consequences. Not to mention, from a historical perspective, countries like the U.S. have only benefited from low trade barriers and economic integration. For these reasons, we don’t think a trade war is likely, but given potential consequences, it is something that we will be closely monitoring.

Portfolio Review and Updates

Global and Sector Diversification Helped Portfolios

In 2017, global diversification added to portfolio returns, and so far this year, it has helped mitigate losses particularly within bonds, real estate, and infrastructure stocks. Having an international allocation within these asset classes has helped buffer the impact of rising interest rates in the U.S. Further, investing a significant portion of one’s portfolio in stocks and bonds of companies and countries outside the U.S. offers diversification to a broader segment of economic and market forces, which produce returns that can vary from those of U.S. asset classes. We believe that optimal diversification means taking a strategic global approach.

Sector diversification has also helped portfolios recently, particularly in the U.S. with the recent sell-off in technology and energy pipeline stocks. Although our client portfolios have an allocation to technology stocks, our smaller-cap and value-oriented tilt has helped to limit the declines from some of the big technology companies in the U.S. that had been trading at lofty valuation levels. Similarly, while our client portfolios have an allocation to energy pipeline stocks, they are spread across other “alternative” or “real” asset classes as well, to help mitigate losses in any one of these areas. We still believe in the merits of alternative asset classes when done with broad-based allocations.

A Disciplined Approach is Best During Times Like This

Managing a portfolio in a disciplined manner and sticking to one’s long-term investment plan usually results in better outcomes during (and long after) market conditions like this. Considering our outlook that markets are inevitably going to recover given solid fundamentals, we think one should consider accelerating the investment of available cash into both stocks and bonds during market declines—such as the ones we’ve experienced this year—to achieve target asset allocations. As usual, for portfolios that are already fully invested, we are monitoring and rebalancing those that have materially deviated from their target.

Sources

¹The World Bank, Open Data Search

Important Disclosure Information

Please remember that different types of investments involve varying degrees of risk, including the loss of money invested. Past performance may not be indicative of future results. Therefore, it should not be assumed that future performance of any specific investment or investment strategy, including the investments or investment strategies recommended or undertaken by Capstone Financial Advisors, Inc. (“Capstone”) will be profitable. Definitions of any indices listed herein are available upon request. Please remember to contact Capstone if there are any changes in your personal or financial situation or investment objectives for the purpose of reviewing our previous recommendations and services, or if you wish to impose, add, or modify any reasonable restrictions to our investment management services. This article is not a substitute for personalized advice from Capstone and nothing contained in this presentation is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Investment decisions should always be based on the investor’s specific financial needs, objectives, goals, time horizon, and risk tolerance. This article is current only as of the date on which it was sent. The statements and opinions expressed are, however, subject to change without notice based on market and other conditions and may differ from opinions expressed by other businesses and activities of Capstone. Descriptions of Capstone’s process and strategies are based on general practice, and we may make exceptions in specific cases. A copy of our current written disclosure statement discussing our advisory services and fees is available for your review upon request.