Investment Perspective Q3 2018: What would be the economic impact of tariffs?

Key Points:

In 2018, stocks have been held back mainly by concerns about trade tensions. Bonds in the U.S. have declined modestly because of rising U.S. interest rates, while international bonds have appreciated as foreign rates have remained steady. We expect stock returns to be better the rest of the year and bond returns to finish positive, even though they continue to be challenged.

The U.S. economy is going through a growth spurt driven by strong consumer spending, combined with tax cuts and new government spending plans. Meanwhile, economic recoveries continue abroad; Europe, however, still faces many challenges. We still expect global economic growth to remain on track. Risk of trade war has increased but is still not likely.

Late-cycle conditions typically result in higher market volatility with lower returns. Investing in high quality bonds will be an effective way to manage portfolio risk going forward. Controlling costs within investment portfolios will be critical going forward to capture (and keep) as much of the returns that markets deliver.

Trade Tensions Suppress Stock Market Returns

Contrary to 2017—a year of synchronized global growth, low inflation, and low volatility, which led to high returns for stocks around the world—the first half of 2018 has been more of a mixed bag. (See Figure 1.) Although the corporate earnings and economic growth pictures are still bright overall, sentiment has dampened mainly due to concerns about trade tensions. So far this year, the result has been lower stock market returns with higher volatility. We are not surprised to see this kind of activity. In fact, we expect it to continue (regardless of the attention-grabbing headlines that come) given that we are in the later stages of the current economic cycle.

Similar to stocks, bond returns have been lackluster in 2018, but for different reasons. Firming inflation and accelerating economic growth in the U.S. prompted the Federal Reserve (the Fed) to raise interest rates twice so far this year. Because bond prices go down when interest rates move up, U.S. bond returns have been modestly negative so far in 2018. In contrast, because most major foreign central banks have held their rates steady due to moderating economic growth abroad, international bond returns have been positive. We expect interest rates to continue to move up gradually, but we think the Fed is more than halfway done.

Market Returns Should Be Better the Rest of the Year

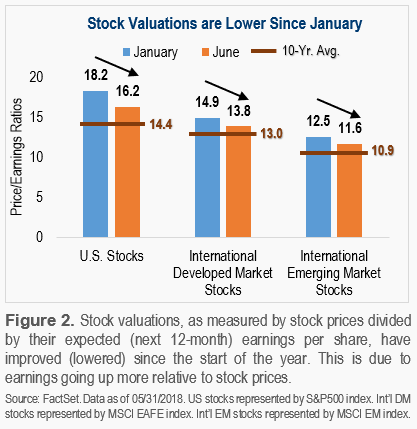

The fundamental backdrop for stocks remains favorable, with strong corporate profit growth driven by a healthy global economy. Earnings growth has improved stock valuations recently. (See Figure 2.) Although current geopolitical issues are likely to cause market volatility, we expect stock returns to improve throughout the remainder of the year. Bond returns, on the other hand, should still be challenged. However, we think bond prices have already been (mostly) reflective of investor expectations concerning potential rate hikes later this year (and next year). Assuming central banks stay on course with the plans they’ve communicated, bonds will likely finish the year with positive returns.

The U.S. Economy Continues to Look Healthy

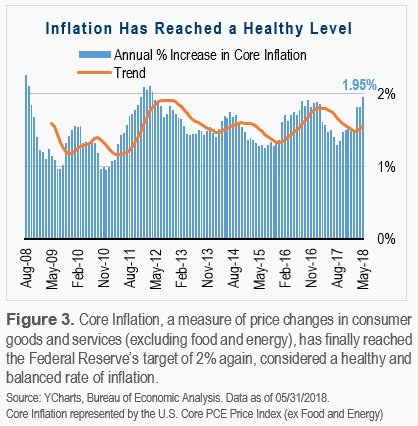

Economic data so far this year has indicated that the U.S. economy is going through a growth spurt. Although it is unclear how long it will last, this growth is being driven by strong consumer spending, combined with tax cuts and government spending plans that have helped to offset the dampening impact of interest rate increases. According to the Fed’s latest statements, it expects to gradually raise rates two more times this year and possibly three times next year. The Fed feels confident in doing this because the job market remains strong, and inflation has finally reached the Fed’s target of 2% with no signs of overheating. (See Figure 3.)

Europe Has Experienced a Mild Setback

Outside of the U.S., economic recoveries continued across Europe and Asia. Recent economic data coming out of Europe, however, has indicated that growth has softened relative to the start of the year. There are many challenges that Europe still faces. The 19-country eurozone still struggles with political fragility; the rise of populism in Italy is the latest example. Immigration tensions throughout the eurozone raise the risk of European fragmentation, albeit a low risk still. Likewise in the UK, uncertainty remains about the potential impact of “Brexit.” However, the strength of the global economy, together with still supportive central banks, should help underpin the recovery in Europe.

Global Economic Growth Will Likely Remain on Track

We still expect global economic growth (U.S. and abroad) to continue and moderately accelerate throughout the year. Despite recent headlines about tariffs and the resulting market reactions, almost all the various economic indicators we monitor are still trending in a positive direction, and there are no imminent signs of a global recession. While challenges abroad persist (particularly throughout Europe), central banks remain patient and accommodative. With the U.S. economy further along, the recently passed tax cuts and government spending plans should help continue to offset increasing interest rates.

Risk of Trade War Has Increased But is Still Not Likely

Recent announcements by the Trump Administration on the imposition of tariffs on imports from China, Canada, Mexico and Europe has undoubtedly increased the likelihood of a trade war. However, given our expectations of minimal direct economic impact from the tariffs, we still don’t think long-term investors should be overly concerned at this point. Despite the expansion of the new tariff announcements (beyond China and industrial goods), the potential impact on trade and the global economy remains limited. The amount of imports currently in question still represent small fractions of trade (and gross domestic product) between the U.S. and other countries.

Targeted bilateral tariffs (tariffs that are imposed on each other by two different nations) will likely continue, but we believe that the outcome will be a renegotiation of existing trade deals. It is in no country’s best interest to impose tariffs and raise trade barriers. Tariffs are inflationary (because they raise the price of imports) and can force central banks to raise interest rates sooner than they otherwise would have planned. Protectionist trade policies, which restrict imports from other countries, will likely slow corporate activity and potentially crimp global growth.

Financial markets serve as a leading indicator for the economy. So far this year, stocks have reacted negatively to trade tensions in the form of subdued returns, while bonds have declined partly on concerns of rising inflation expectations. These market reactions validate the potential risks of a trade war. Although the likelihood of a global trade war has increased, we don’t think it will happen. Still, given potential consequences, it is something that we continue to monitor closely.

Portfolio Review and Updates

Higher interest rates have presented opportunity

Diversification has helped mitigate recent declines within bonds caused by rising U.S. interest rates. We diversify portfolio bond allocations in three main ways: 1) Investing across all maturities (i.e., short, intermediate, and long-term bonds). 2) Investing across major bond asset classes (i.e., government, corporate, securitized, and municipal bonds). 3) Investing globally. We expect this this type of diversification to continue to buffer against potential future interest rate hikes regardless of when, and how quickly they happen.

We continue to believe that long-term investors should hold bonds for income and to achieve a return above the rate of inflation. In fact, today’s rising interest rate environment has presented us the opportunity to “lock in” bonds that pay higher coupons. Disciplined rebalancing and reinvestment of income have allowed us to do this in client portfolios. Additionally, our bonds funds continuously reinvest in higher coupon securities over time. This has been (and will continue to be) beneficial for long-term investors.

Late-cycle conditions warrant strategic portfolio design

Investing in high quality bonds will be an effective way to manage portfolio risk going forward. High quality bonds are issued by governments, municipalities, and corporations that are stable and very unlikely to default. These types of bonds tend to be a better ballast to offset stock volatility, which tends to be higher in the later stages of an economic cycle. As such, we have been improving the quality of bond allocations with the goal to proactively position portfolios to better withstand potential future downturns.

Controlling costs within investment portfolios will be critical going forward to capture (and keep) as much of the returns that markets deliver. Absent significant acceleration in economic growth, our expectations for future market returns is that they will be lower than in recent years. Lower market returns are not unusual in the later stages of an economic cycle. As such, we believe that building portfolios with cost-efficient and tax-efficient investments will help investors achieve more of their return goals in the years ahead.

Important Disclosure Information

Please remember that different types of investments involve varying degrees of risk, including the loss of money invested. Past performance may not be indicative of future results. Therefore, it should not be assumed that future performance of any specific investment or investment strategy, including the investments or investment strategies recommended or undertaken by Capstone Financial Advisors, Inc. (“Capstone”) will be profitable. Definitions of any indices listed herein are available upon request. Please remember to contact Capstone if there are any changes in your personal or financial situation or investment objectives for the purpose of reviewing our previous recommendations and services, or if you wish to impose, add, or modify any reasonable restrictions to our investment management services. This article is not a substitute for personalized advice from Capstone and nothing contained in this presentation is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Investment decisions should always be based on the investor’s specific financial needs, objectives, goals, time horizon, and risk tolerance. This article is current only as of the date on which it was sent. The statements and opinions expressed are, however, subject to change without notice based on market and other conditions and may differ from opinions expressed by other businesses and activities of Capstone. Descriptions of Capstone’s process and strategies are based on general practice, and we may make exceptions in specific cases. A copy of our current written disclosure statement discussing our advisory services and fees is available for your review upon request.