New Tax Rules for Charitable Giving Start in 2026—Here's What to Consider Now

Key Points:

The One Big Beautiful Bill Act (OBBBA) substantially changes the tax landscape for charitable giving, providing new benefits and limitations.

Provisions that limit the benefits for individual and corporate donors don’t take effect until 2026, creating a significant opportunity to accelerate giving into 2025.

Depending on one’s long-term charitable giving goals, they may want to consider bunching multiple years’ worth of charitable donations into a single year.

Understanding the One Big Beautiful Bill Act (OBBBA)

The One Big Beautiful Bill Act (OBBBA) is poised to reshape key areas of the tax code, including how Americans receive deductions for charitable contributions. While many provisions take effect in 2026, donors—especially high earners—should start evaluating their giving strategies now.

The Act aims to broaden participation in charitable giving while reducing the relative tax advantages for large donors. In practice, this means many households could see smaller federal tax deductions for the same level of generosity starting in 2026.

What’s Changing for Charitable Giving in 2026

A 0.5% AGI “Floor” on Deductions

Beginning in 2026, charitable deductions will apply only to contributions exceeding 0.5% of adjusted gross income (AGI), for individuals who itemize their deductions.

If your AGI is $1 million, the first $5,000 of charitable gifts would not be deductible. For donors who make regular annual gifts, this “floor” reduces the cumulative tax benefit of ongoing contributions.

A 35% Cap on Deduction Value

The OBBBA also caps the effective tax benefit of itemized charitable deductions at 35% per dollar donated.

Today, top-bracket taxpayers can deduct gifts at up to 37% of their marginal rate. The 2% difference might seem modest, but for large donations it adds up.

How will this play out in practice?

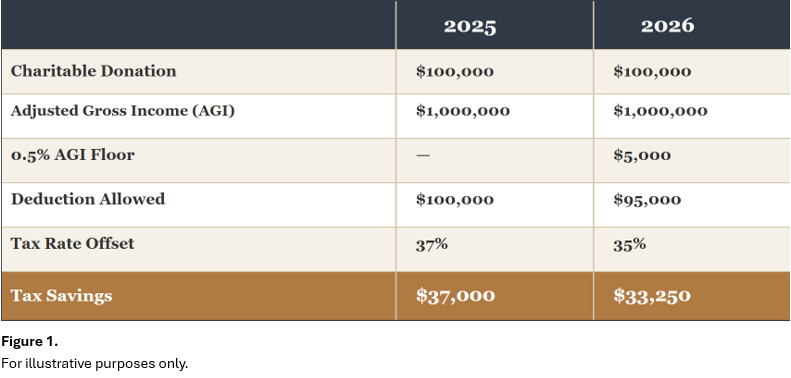

Consider the following example: If your AGI is $1 million and you make a $100,000 charitable gift in 2025, the full $100,000 gift is deductible against the 37% federal income tax rate, for a tax benefit of $37,000. (See Figure 1 below.) Under the new law, starting in 2026, the tax benefit will drop—you’ll only be able to deduct $95,000, with a reduced tax offset rate of 35%. As a result, the tax savings from a $100,000 donation will decline from $37,000 in 2025 to $33,250 in 2026.

These changes could reduce after-tax giving efficiency—unless donors plan strategically in advance.

Why 2025 May Be the Year to Give

With these new rules approaching, 2025 offers a final window to take advantage of today’s more favorable deduction framework. Accelerating or “bunching” multiple years of charitable gifts into 2025 could help maximize the deduction value while it’s still available at higher rates. Moreover, with stock markets near all-time highs, donating appreciated securities would help to avoid capital gains taxes while maximizing the impact of your charitable giving.

The Strategy of “Bunching”

“Bunching” involves combining several years’ worth of donations into a single tax year to exceed the standard deduction threshold and unlock greater itemized benefits.

For example, rather than giving $50,000 annually in 2025 and 2026, a donor might contribute $100,000 in 2025, capture the full deduction now, and then resume normal giving in later years.

This strategy aligns especially well with the temporary state and local tax (SALT) deductions cap relief in 2025, which raises the state and local tax deduction limit from $10,000 to $40,000 for joint filers (with phaseouts above $500,000 of income). Together, these changes could make itemizing more attractive in 2025 compared to 2026

Leveraging Donor-Advised Funds (DAFs)

For donors who wish to capture a 2025 deduction without rushing to choose recipient charities, Donor-Advised Funds (DAFs) offers a solution.

By contributing to a DAF before year-end, donors can:

Claim the full deduction in 2025 under current rules.

Distribute funds over time to individual charities in future years.

Retain investment flexibility for assets held in the fund.

DAFs provide both timing and strategic advantages—especially useful for those in a high income tax year that want to plan for multi-year philanthropic goals in the future.

The Role of IRA Qualified Charitable Distributions (QCDs)

For donors aged 70½ or older, IRA Qualified Charitable Distributions (QCDs) remain one of the most tax-efficient giving vehicles available.

Up to $108,000 per year can be transferred directly from an IRA to a qualified public charity—without counting as taxable income. QCDs effectively bypass the AGI floor and the 35% deduction cap, preserving full tax efficiency even after 2026.

They also help satisfy Required Minimum Distributions (RMDs), making them a dual-purpose tool for retirees seeking both impact and tax control.

Corporate Giving Rules Tighten

Businesses will face stricter standards too. Starting in 2026, corporate charitable deductions will apply only to donations exceeding 1% of taxable income, with the overall deduction cap remaining at 10%.

Corporate leaders may want to evaluate their philanthropic budgets in 2025 to lock in current treatment and maintain flexibility for larger gifts in the future.

Bringing It All Together: Planning with Purpose

The OBBBA’s charitable deduction reforms highlight an important reality:

Even when tax rules change, thoughtful planning creates opportunity.

2025 represents a strategic year for donors to:

Reassess giving patterns and timing.

Utilize DAFs or QCDs to preserve tax efficiency.

Coordinate charitable strategies with broader estate and tax goals.

By engaging early with financial and tax advisors, donors can align generosity with tax efficiency—maximizing both impact and intention.

Start planning now to make your 2025 charitable giving go further — connect with your Capstone advisor or visit our Contact Us page to explore your strategy.

FAQ

1. What is the One Big Beautiful Bill Act (OBBBA)?

It’s a new tax law taking effect in 2026 that changes how charitable deductions work. The goal is to simplify the tax code, but it could reduce the size of deductions for some donors.

2. What’s changing for charitable deductions?

Two main things:

Only donations above 0.5% of your income will count for deductions.

The tax benefit per dollar donated will be capped at 35%, down from today’s 37%.

3. Why does 2025 matter so much?

2025 is the last year under current rules. Making larger or “bunched” donations before the new limits start could help you get a bigger tax benefit for the same level of giving.

4. What does “bunching” mean?

“Bunching” means combining several years’ worth of donations into one tax year.

For example, instead of giving $50,000 each year in 2025 and 2026, you could give $100,000 in 2025 to take advantage of the current deduction rules.

5. What is changing with the SALT deduction in 2025?

The SALT deduction cap will rise from $10,000 to $40,000 for joint filers in 2025. For many taxpayers, this temporary increase could make itemizing more valuable and enhance the benefit of larger charitable contributions that year.

6. How can Donor-Advised Funds (DAFs) help?

DAFs let you make a large donation now, claim the tax deduction, and give the money to charities over time. It’s a smart way to lock in current tax benefits while spreading out your charitable impact.

7. What about giving through my IRA?

If you’re 70½ or older, you can donate up to $108,000 each year directly from your IRA to qualified charities. These Qualified Charitable Distributions (QCDs) skip the new limits and don’t add to your taxable income.

8. Are businesses affected too?

Yes. Starting in 2026, companies can only deduct donations above 1% of taxable income, with an overall cap of 10%. Some may want to make larger gifts in 2025 to use the current rules.

9. How should I prepare?

Review your giving plans with your financial and tax advisors now. 2025 could be the right time to bunch donations, open a DAF, or make IRA gifts for maximum benefit.

10. Who can help me plan my charitable strategy?

Your Capstone advisor can help you build a giving plan that fits your financial goals and the coming tax changes. Visit our Contact Us page to start the conversation.

Disclosures:

This article is not a substitute for personalized advice from Capstone and nothing contained in this presentation is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. This article is current only as of the date on which it was sent. The statements and opinions expressed are, however, subject to change without notice based on market and other conditions and may differ from opinions expressed by other businesses and activities of Capstone. Descriptions of Capstone’s process and strategies are based on general practice, and we may make exceptions in specific cases. A copy of our current written disclosure statement discussing our advisory services and fees is available for your review by contacting us at capstonefinancialadvisors@capstone-advisors.com or (630) 241-0833.