What Actually Matters For Markets During Geopolitical Shocks?

KEY POINTS:

Markets began the quarter on stable footing before geopolitical tensions shifted sentiment, leading to a pullback in stocks and rising interest rates that weighed on bonds. Looking ahead, returns may be more measured as valuations remain elevated and policy uncertainty persists, with bonds providing income and potential stability and stock market leadership likely to broaden as gains become less concentrated.

The U.S. economy continued to expand at a slower pace, supported by steady consumer spending and a still-solid labor market, while inflation became less consistent amid rising energy costs and uneven global growth. Growth should remain moderate, with inflation trending lower over time despite near-term volatility as central banks respond to shifting inflation and labor market trends.

Investors are focused on how geopolitical events—particularly in the Middle East—may influence markets through energy prices, inflation, and interest rates. We explore why markets tend to respond more to the economic impact of these events than the headlines, and how the duration and scale of disruptions shape market outcomes beneath the surface.

Recent market behavior reinforces the importance of building portfolios that can withstand a range of outcomes rather than relying on any single driver of returns. A diversified approach across stocks, bonds, real assets, and select private investments can help manage risk while capturing opportunities as conditions evolve.

MARKET REVIEW

GEOPOLITICS SHIFTED MARKET TONE

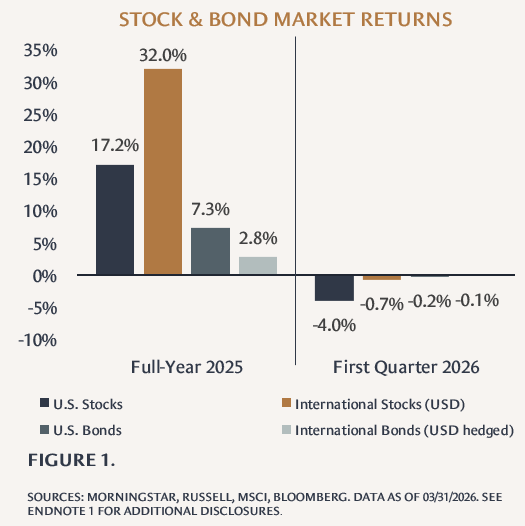

Markets began the first quarter on relatively stable footing, supported by steady earnings and a still-constructive policy backdrop, before sentiment shifted meaningfully late in the period. Escalating conflict in the Middle East, centered on Iran, introduced a more pronounced risk-off tone, increasing volatility and weighing on both stocks and bonds (see Figure 1). This marked a clear change in market behavior, as geopolitical developments—rather than economic or earnings data—became the primary driver of investor sentiment.

STOCKS REPRICED AMID RISING UNCERTAINTY

Global stocks pulled back after reaching elevated levels earlier in the quarter, reflecting geopolitical uncertainty and valuation pressure, as expectations around growth and policy shifted and scrutiny on earnings—particularly in technology and AI-related companies—increased. The late-quarter selloff was broad-based across company sizes and investment styles, though leadership trends over the full period showed early signs of rotation, with mid- and small-cap stocks outperforming large caps and value stocks outpacing growth. International markets declined more sharply during the selloff but still finished the quarter ahead of U.S. stocks, reflecting differences in market composition—particularly the heavier weighting of technology-related companies in the U.S.—which declined materially during the period.

ENERGY AND INFLATION DROVE BOND WEAKNESS

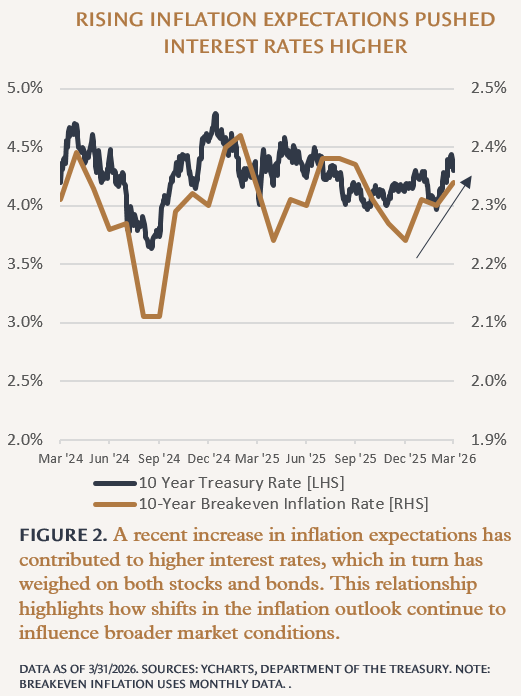

The most influential cross-asset development was a sharp rise in energy prices, driven by supply disruptions tied to geopolitical tensions. Higher oil prices lifted inflation expectations and led to a broad repricing of interest rates, with yields moving higher and weighing on bond returns (see Figure 2). This renewed focus on inflation marked a reversal from earlier optimism around moderating price pressures, reinforcing the sensitivity of both stocks and bonds to changes in the inflation outlook and the expected path of policy.

MARKET OUTLOOK

RETURNS MAY MODERATE AS EXPECTATIONS RESET

Stock market returns are likely to be more measured in the period ahead, reflecting a combination of elevated valuations and a more uncertain backdrop for earnings and policy. Corporate profits should continue to grow, supported by resilient consumer and business activity, but markets may be more sensitive to whether those expectations are met or exceeded. This could lead to a less consistent path forward, with periodic pullbacks tied to earnings results, interest-rate expectations, or shifts in investor sentiment.

VOLATILITY LIKELY TO REMAIN ELEVATED AMID POLICY UNCERTAINTY

Monetary policy and interest rates are likely to remain central drivers of both stock and bond market outcomes. While the broader direction of policy still points toward easing over time, the path may be uneven as inflation risks—particularly those linked to commodity-driven and geopolitical pressures—complicate central bank decisions and shift expectations for the timing of rate cuts. As a result, interest rates could remain higher for longer than previously expected, contributing to ongoing rate volatility and influencing both stock valuations and bond market returns, even if any inflationary pressures from these disruptions prove temporary.

BOND INCOME SHOULD REMAIN ATTRACTIVE WHILE STOCK LEADERSHIP BROADENS

Bonds should continue to offer a more balanced return profile, with current yields providing meaningful income and a potential cushion during periods of market stress. At the same time, stock market leadership could gradually broaden beyond large-cap companies as earnings growth becomes less concentrated, with the benefits of continued investment in areas such as artificial intelligence increasingly extending across sectors and to a wider range of company sizes. On the global front, this broadening in earnings growth and market leadership could also extend across regions, as a narrowing gap in growth, inflation, and policy supports improved earnings prospects and a more balanced contribution to returns outside the U.S.

ECONOMIC REVIEW

GROWTH REMAINED RESILIENT BUT SLOWED

Economic activity continued to expand during the first quarter, though the pace of growth moderated. In the U.S., consumer spending remained the primary driver, supported by steady income growth and a still-solid labor market, while business investment was more mixed outside of ongoing spending tied to artificial intelligence and related infrastructure. Abroad, momentum softened more noticeably, particularly in Europe and Japan, where higher energy costs and weaker industrial activity weighed on growth. Overall, the period reflected a shift from stronger, above-trend expansion toward a more measured pace.

INFLATION TRENDS BECAME UNEVEN

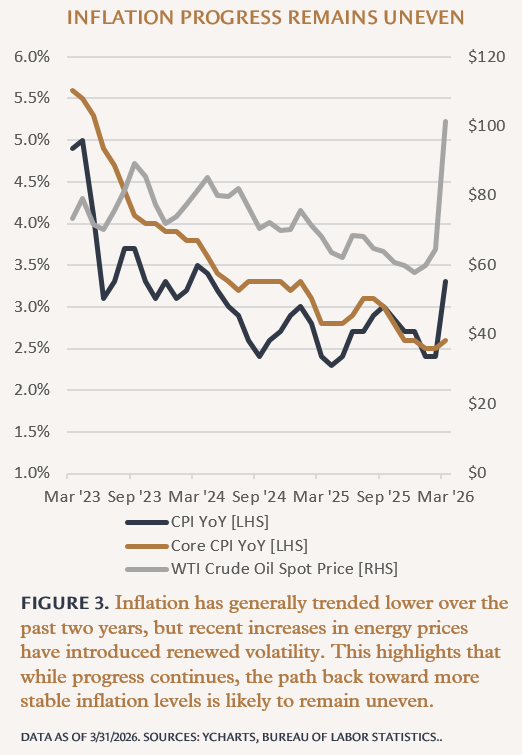

Progress on lowering inflation became less consistent as energy prices moved higher, driven in part by geopolitical tensions involving Iran that disrupted supply expectations and trade flows. This added renewed upward pressure to headline inflation, even as underlying price trends in goods and services remained relatively stable. In the U.S., earlier progress had been encouraging, but the rebound in energy-related costs highlighted how sensitive inflation can be to external shocks, with higher energy costs also weighing on household purchasing power and business margins. The quarter reinforced that the path toward bringing inflation back toward target levels is likely to remain uneven (see Figure 3).

LABOR MARKETS COOLED WHILE POLICY PAUSED

Labor market conditions in the U.S. remained solid but showed early signs of cooling. Hiring activity slowed, job openings declined, and unemployment edged modestly higher, though layoffs remained limited. Similar, though more uneven, trends were observed abroad. Against this backdrop, central banks largely held policy rates steady, balancing renewed inflation pressures with evidence of moderating growth. In the U.S., rising government spending and borrowing needs continued to place pressure on public finances, adding another layer of complexity to the policy environment.

ECONOMIC OUTLOOK

GROWTH SHOULD REMAIN STEADY BUT COOLING

Economic growth should continue at a moderate pace, with recent data suggesting a slowing but still expanding backdrop, supported by ongoing consumer spending and a labor market that remains stable even as it gradually slows. Household spending should remain a key support, though likely at a more measured pace, and businesses may grow more selective with hiring and investment as borrowing costs remain elevated and businesses prioritize efficiency and capital discipline. Outside the U.S., improving conditions in parts of Europe and emerging markets could provide some support, though growth will likely differ across regions based on local policy decisions and the strength of consumer demand.

INFLATION SHOULD EASE GRADUALLY WITH SOME STICKINESS

Inflation should trend lower over time, though the path back toward central bank targets may be uneven. Areas like housing, healthcare, and other service-based categories are likely to remain more persistent, while energy prices could move up or down alongside geopolitical developments. Overall, inflation should trend in the right direction, but progress may come more slowly and with occasional setbacks.

POLICY AND LABOR MARKETS SHOULD NORMALIZE GRADUALLY

Central banks should remain cautious as they balance moderating inflation with an economy that continues to expand. Interest rate decisions will likely remain closely tied to incoming data, particularly around inflation and employment. Labor markets should continue to ease in a measured way, with slower job growth and more moderate wage gains helping to reduce inflation pressures without a sharp rise in unemployment. At the same time, developments in energy markets and geopolitical tensions—particularly in the Middle East—remain important variables that could influence both inflation and growth in the months ahead.

ON THE MINDS OF INVESTORS

WHAT ACTUALLY MATTERS FOR MARKETS DURING GEOPOLITICAL SHOCKS?

The recent escalation involving Iran has understandably raised investor concern, particularly given its potential to disrupt a critical region for global energy supply. Headlines around military conflict and regional instability can feel inherently market-moving, and in the short term, they often are. But history suggests that markets rarely respond to geopolitical events based on the headlines alone—instead, they focus on how, and to what extent, those events affect the underlying economic backdrop.

MARKETS RESPOND TO ECONOMIC IMPACT, NOT HEADLINES

The most important transmission mechanism in situations like this is energy. When conflict threatens oil production or transportation routes, energy prices can rise, which in turn can influence inflation, consumer spending, and business costs. That ripple effect is what ultimately drives market outcomes—not the event itself, but whether it meaningfully alters the path of inflation, interest rates, or corporate earnings. If those economic channels remain relatively stable, market reactions tend to be contained, even amid elevated geopolitical tension

DURATION AND SCALE DRIVE MARKET IMPACT

Just as important as the initial shock is how long it lasts and how far it spreads. Short-lived disruptions—while unsettling—have historically had limited lasting impact on markets, particularly when supply adjusts or tensions de-escalate. More sustained or broad-based disruptions, especially those that keep energy prices elevated over time, are more likely to influence inflation trends, central bank policy, and, if prolonged, broader economic growth. In other words, markets tend to be less focused on the existence of conflict and more focused on whether it creates persistent economic pressure.

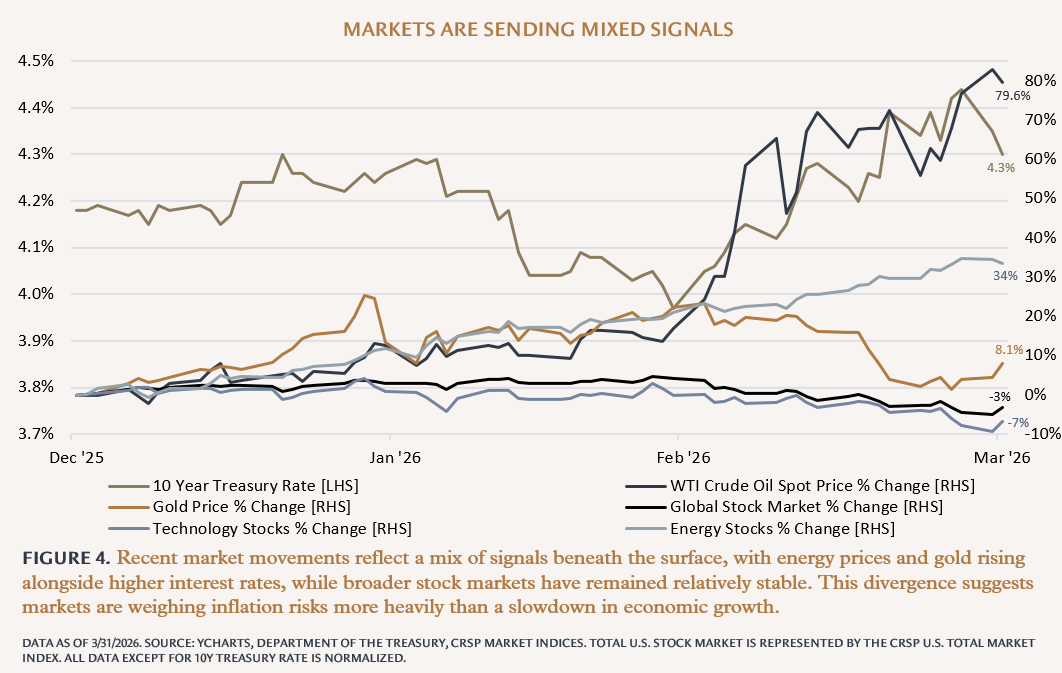

MARKET SIGNALS ARE MIXED BENEATH THE SURFACE

Markets are reflecting multiple, and sometimes conflicting, signals (see Figure 4). In the current environment, energy prices have moved higher and gold has strengthened, reflecting concern around potential supply disruption and inflation. At the same time, bond yields have risen rather than fallen, suggesting markets are weighing the risk of higher inflation more than a slowdown in growth.

Meanwhile, broad stock market indexes have remained relatively stable, indicating that markets are not yet pricing in a lasting disruption to corporate earnings. Beneath the surface, however, leadership has diverged—energy, materials, and utilities have generally moved higher, while more economically sensitive areas such as consumer-oriented companies and financials have come under pressure. These crosscurrents help explain why headline market moves may not fully capture what is happening underneath.

STAYING FOCUSED ON FUNDAMENTALS

For long-term investors, the key takeaway is not to dismiss geopolitical risks, but to keep them in proper context. Markets have navigated many such events over time, and while they can introduce periods of volatility, their lasting impact has typically depended on whether they alter the broader economic and earnings environment. Maintaining a disciplined perspective—grounded in fundamentals rather than headlines—remains one of the most effective ways to navigate periods of uncertainty.

PORTFOLIO MANAGEMENT

BUILD PORTFOLIOS THAT CAN WITHSTAND DIFFERENT OUTCOMES

Recent market behavior has reinforced that portfolio outcomes are being driven by a wider set of factors, rather than any single, consistent relationship between asset classes over time. No single asset class or investment theme consistently offsets another across all environments. This underscores the importance of building portfolios that incorporate a range of return drivers—including stocks, bonds, real assets, and select private investments—so that performance is not dependent on any one outcome.

AVOID OVERRELIANCE ON A NARROW SET OF DRIVERS

While a relatively small group of companies continues to drive a meaningful share of market returns, recent volatility has shown that leadership can shift and broaden over time. Performance has varied more across sectors, regions, and company sizes as expectations around growth and innovation evolve. Maintaining diversified exposure helps reduce dependence on any single theme and allows portfolios to participate more broadly as leadership changes.

USE BONDS FOR INCOME AND STABILITY OVER TIME

Bonds continue to serve an important role in portfolios by providing income and generally lower volatility than stocks. With yields still at relatively attractive levels, they remain a meaningful source of income within diversified portfolios. Periods where stocks and bonds move in the same direction—particularly when inflation expectations are rising—can challenge their diversification benefit in the short term. However, in environments characterized by slowing growth or economic stress, bonds have historically provided stability and support, reinforcing their role as a diversifier to stocks over time within a balanced portfolio.

INCLUDE REAL ASSETS TO ADDRESS INFLATION UNCERTAINTY

In environments where inflation outcomes are less predictable, assets tied to real economic activity—such as infrastructure and real estate—can provide additional diversification. These investments may offer income and some sensitivity to inflation, with returns supported by underlying cash flows and real asset usage, complementing traditional stock and bond allocations. Including them within a broader portfolio can help address risks that are not fully captured by public markets alone.

SIZE PRIVATE INVESTMENTS WITH LIQUIDITY IN MIND

Private market investments can offer access to differentiated return streams and long-term opportunities not always available in public markets. However, recent developments have highlighted the importance of understanding liquidity structures and investor behavior during periods of stress. Aligning these investments with long-term time horizons and sizing them appropriately remains critical to their effectiveness within a portfolio.

STAY DISCIPLINED THROUGH SHORT-TERM UNCERTAINTY

Geopolitical events and shifting market narratives can create periods of volatility that are difficult to anticipate or respond to effectively. Rather than adjusting portfolios based on short-term developments, a more durable approach is to remain anchored to a well-diversified, long-term strategy. Over time, consistency in approach has been a more reliable driver of outcomes than reacting to individual events.

FAQs

Q: What drove stock and bond markets this quarter?

Markets began on stable footing but shifted as geopolitical tensions in the Middle East affected sentiment and increased volatility. Rising energy prices pushed inflation expectations higher, leading to higher interest rates that weighed on bonds and pressured stock valuations. This highlighted how quickly markets can respond when inflation and policy expectations change.

Q: Why did bonds struggle despite their role as a stabilizer?

Bond returns were challenged as interest rates moved higher in response to rising inflation expectations, particularly from energy price increases. When inflation concerns resurface, yields tend to rise, which can pressure bond prices in the short term. This dynamic reflects bonds’ sensitivity to changes in the inflation outlook and policy expectations.

Q: Are current stock market valuations a concern?

Valuations remain elevated, which may lead to more measured returns and greater sensitivity to earnings and policy developments. This does not necessarily signal a negative outcome, but it does mean markets may react more noticeably to shifts in expectations. Elevated valuations often reflect both strong current fundamentals and optimism about future growth.

Q: Why has market leadership been so concentrated?

A relatively small group of companies—many tied to artificial intelligence—has driven a significant share of market returns. This reflects both strong earnings growth and high expectations for continued innovation. However, concentrated leadership can make markets more sensitive to changes in sentiment or questions around future growth.

Q: Could market leadership begin to broaden from here?

There are early signs that performance may become less concentrated across company sizes, sectors, and regions. As earnings growth extends beyond a narrow group of companies, a wider set of stocks may contribute to returns. This type of broadening is a common feature as market cycles evolve.

Q: How do geopolitical events actually affect markets?

Markets tend to respond less to headlines and more to the economic impact of geopolitical events. The key channel is often energy prices, which can influence inflation, interest rates, and corporate earnings. The duration and scale of disruptions typically determine whether market effects are short-lived or more persistent.

Q: What is happening with inflation right now?

Inflation trends have become less consistent, with energy prices contributing to renewed upward pressure even as underlying trends remain relatively stable. While inflation is expected to trend lower over time, the path may be uneven. External factors like geopolitical developments can create short-term volatility in inflation readings.

Q: How are interest rates likely to evolve?

Interest rates are expected to remain an important driver of both stock and bond markets, with central banks balancing moderating growth and uneven inflation. While the broader direction may still point toward easing over time, the path could be uneven. This may result in continued rate volatility as expectations adjust.

Q: Is the economy still on solid footing?

Economic growth has remained resilient, supported by consumer spending and a still-solid labor market, though the pace has moderated. Labor markets are gradually cooling, and business activity has become more selective. Overall, the economy appears to be transitioning toward a more measured and sustainable pace of growth.

Q: How do global trends compare to the U.S.?

Growth outside the U.S. has been more uneven, with some regions facing greater pressure from higher energy costs and weaker industrial activity. However, improving conditions in certain areas could support more balanced global growth over time. Differences in inflation, policy, and economic momentum may continue to drive variation across regions.

Q: What does this environment mean for diversified portfolios?

Recent market behavior shows that no single asset class consistently offsets another in all environments. A mix of stocks, bonds, real assets, and select private investments can help provide multiple sources of return and manage risk across different conditions. Diversification remains a key principle when market drivers are shifting.

Q: What role should bonds, real assets, and private investments play today?

Bonds continue to offer income and can provide stability over time, particularly during periods of slowing growth. Real assets such as infrastructure and real estate may help address inflation uncertainty through income and sensitivity to economic activity. Private investments can offer differentiated return streams, though they should be aligned with long-term time horizons and liquidity needs.

SOURCES & ENDNOTES

1 Notes: U.S. Stock returns are represented by the Russell 3000 Index Total Return (TR) USD. International Stock returns are represented by the MSCI All-Country-World Ex-USA Investible Market Index (IMI) Gross Return (GR) USD. U.S. Bond returns are represented by the Bloomberg Aggregate Bond Index Total Return (TR) USD. International Bond returns are represented by the Bloomberg Global Aggregate Ex-USA Dollar-Hedged Index Total Return (TR) USD. Past performance is not indicative of future results.

IMPORTANT DISCLOSURE INFORMATION:

Please remember that different types of investments involve varying degrees of risk, including the loss of money invested. Past performance may not be indicative of future results. Therefore, it should not be assumed that future performance of any specific investment or investment strategy, including the investments or investment strategies recommended or undertaken by Capstone Financial Advisors, Inc. (“Capstone”) will be profitable. Definitions of any indices listed herein are available upon request. Please contact Capstone if there are any changes in your personal or financial situation or investment objectives for the purpose of reviewing our previous recommendations and services, or if you wish to impose, add, or modify any reasonable restrictions to our investment management services. This article is not a substitute for personalized advice from Capstone and nothing contained in this presentation is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Investment decisions should always be based on the investor’s specific financial needs, objectives, goals, time horizon, and risk tolerance. This article is current only as of the date on which it was sent. The statements and opinions expressed are, however, subject to change without notice based on market and other conditions and may differ from opinions expressed by other businesses and activities of Capstone. Descriptions of Capstone’s process and strategies are based on general practice, and we may make exceptions in specific cases. A copy of our current written disclosure statement discussing our advisory services and fees is available for your review by contacting us at capstonefinancialadvisors@capstone-advisors.com or (630) 241-0833.