How to Maximize Your Social Security Benefits

Key Points:

The age that you decide to start taking your Social Security benefit can have an enormous impact on how much you end up receiving during your lifetime.

The decision of when to start Social Security benefits should depend on a number of factors including: age, health, genetics, and financial needs.

Life Expectancy, a major unknown factor, also plays a large part in deciding when to file for benefits. We generally recommend an evaluation approach that provides a comparison of benefits over several different scenarios.

According to the Social Security Administration, “Social Security was a major source of income for at least 50% of filing couples and 71% of non-married filers in 2015.”¹ Though these figures have continued to decline each year due to improving savings habits and earnings growth, they show that Social Security continues to play a significant role in most retiree’s income.

Given its relative impact and importance, one of the most common questions we receive from clients is when they should start taking or filing for their Social Security benefit. Since most of us pay into the system throughout our working years, we owe it to ourselves to maximize the amount we get back from Uncle Sam. And although this may seem like a simple question on the surface, the variables that go into finding an appropriate answer add to its complexity. The date that you decide to take your Social Security benefit can have an enormous impact on how much you end up receiving during your lifetime.

Before we delve into the variables that may help you to decide when you should file for Social Security, it is important to highlight the effect that this decision can have on the benefit amount for which you are eligible. For all retirees, the Social Security Administration imposes a mandatory threshold age to receive 100% of their eligible benefit. This is commonly known as your “Full Retirement Age” (FRA). Based upon this age (which can differ depending on your year of birth) and the calculated benefit amount, you can decide to take benefits earlier or later than the FRA date. The earliest you can take benefits is at age 62, which would result in a lower monthly payment than at your FRA. Delaying benefits until after your FRA (age 70 at the latest) is also an option and can result in a higher monthly benefit.

See Figure 1 below, which outlines how the decision of when to begin benefits can have a relative impact on your Social Security income. This “impact” is expressed as a percentage of “Full Retirement Benefits. Depending on your year of birth, taking benefits as early as age 62 can cause your benefit to be reduced by as much as 30% (for those born after 1959), while deciding to wait until age 70 can increase your benefit by as much as 32% (if you were born prior to 1955).

Understanding how taking an early or delayed benefit can affect the amount you receive each month is only a piece of the puzzle when trying to maximize your benefits. How long you are to receive those benefits is another important factor. For this evaluation, considerations that come into play may be your genetics; your overall physical health; improvements in our current healthcare landscape; and your expected financial needs. For those who have poor health or whose genetics show that family lifespans are not as favorable, it may make sense to begin taking benefits earlier than FRA. This would maximize the time horizon during which they are receiving payments, even if those payments are reduced on a monthly basis. The same would apply for those who are forced to retire early or do not have other supplemental assets and may require their Social Security benefits to play a larger role in their monthly budget.

On the other hand, for those who are generally healthier and have evidence that shows a longer family lifespan, waiting to receive benefits can sometimes prove to be more beneficial. Although the benefit payments may be received over less years, the higher monthly payment amounts may make up for the dollars given up from those previous years had benefits been taken earlier. Obviously, for most people, the age at which they will pass away is almost impossible to accurately predict. However, for those who can afford to wait to receive benefits, it could be better in most cases to delay receiving benefits until reaching age 70.

If you are married and your spouse is also eligible for benefits, this further complicates your decision of when you should take your own personal benefit. For many families, one spouse may have to wait for their partner to begin taking benefits before they can start claiming. This is due to the “Deemed Filing Rule” put into effect as a part of the 2015 Bipartisan Budget Act. Under the Deemed Filing Rule, in order for a spouse with a limited earnings record to begin receiving benefits on the other spouse’s record, the primary earner needs to have already applied to begin receiving benefits as well. As a result, the age, health, and financial needs of both family members can influence when and how much in benefits they ultimately receive.

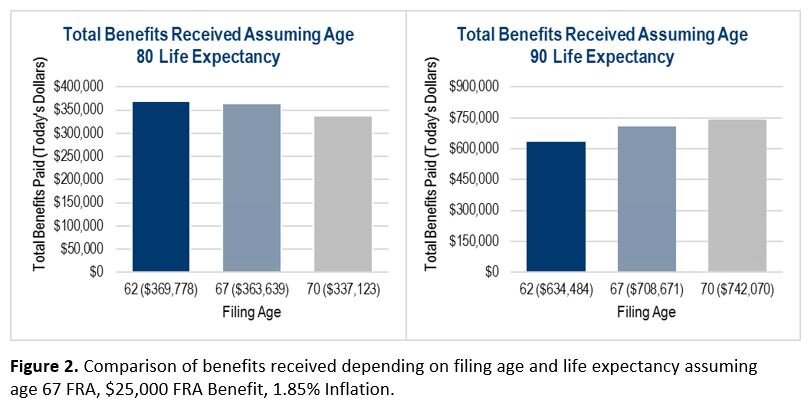

In order to illustrate the timing issue that comes into play when trying to maximize your Social Security benefits, Figure 2 below compares the total lifetime benefits paid between someone with a shorter life expectancy claiming benefits early vs. delaying, and another individual with a longer life expectancy taking benefits early vs. delaying. What you will see from this chart is that for an individual with a life expectancy of age 80 (assuming age 67 FRA), it may make sense to begin taking benefits as early as age 62, while for an individual with a life expectancy of age 90, it would make sense to delay taking benefits until age 70.

We generally recommend an evaluation approach that provides a comparison of benefits over several different scenarios. We recognize that the timing of when you file and how long you live can both have a dramatic impact on the total amount of benefits you receive. As with other areas of your financial planning, taking a look at your entire picture from a holistic sense and using facts such as your overall health; family health and age history; as well as trends in our healthcare system can assist in getting the best possible estimate for life expectancy. This evaluation, along with the consideration of your overall financial needs, can go a long way in helping make a better decision on your needs from Social Security.

Sources

¹https://www.ssa.gov/policy/docs/chartbooks/fast_facts/2017/fast_facts17.pdf Page 14; Relative Importance of Social Security, 2015.

https://www.ssa.gov/planners/retire/applying1.html