Investment Perspective Q2 2019: Yield curve inversion – Is a recession forthcoming?

Key Points:

Stock markets rebounded sharply in the first three months of the year buoyed by growing optimism on a potential U.S.-China trade resolution and global central banks changing tack on rate policy. Despite subsiding stock market volatility, bond markets continued their gains from the end of last year. Stock market returns in 2019 are likely to be strong, and bond returns will likely stay positive.

The U.S. economy has continued to perform well overall. However, outside the U.S. , economic growth across most of the major economies in the world continued to slow. Aggregate global economic growth will likely slow but stay positive in 2019, thereby avoiding a global recession.

Although an important recession gauge briefly flashed a warning sign, there are many other gauges with good track records of predicting recessions that aren’t showing evidence of trouble yet. Although we don’t think a severe recession is imminent, we are further along in the economic cycle and have been making changes to portfolios to further diversify them from stock market risk.

Market Review & Outlook

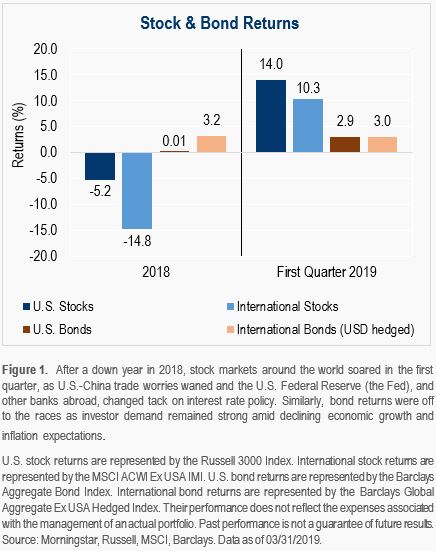

Stocks reverse course on growing optimism

The U.S. stock market rebounded sharply in the first three months of 2019 posting its best quarterly return in almost ten years¹. Similarly, international stocks performed well, reversing course from losses in 2018. (See Figure 1.) These early-year stock market gains were buoyed by growing optimism on a potential U.S.-China trade resolution and new indications from the U.S. Federal Reserve (and other central banks abroad) that interest rate increases in 2019 are off the table. Trade tensions and rising rates were big reasons why stock markets fell in 2018. Therefore, this year’s sharp recovery did not come as a surprise, especially since stocks fell so much and the economy is still healthy.

Bonds gained on slower growth expectations

Despite subsiding stock market volatility, bond markets continued their gains from the fourth-quarter in 2018. Bond interest rates, which fall as bond prices rise, declined around the world due to lower economic growth and inflation expectations. Although the financial markets (both stocks and bonds) usually perform well when interest rates go down, lower rates are a sign that the global economy has started and may continue to slow.

Stocks likely to be strong, bonds to remain positive

Stock market returns in 2019 are likely to be strong given that stocks started the year at low levels after going through bear markets in 2018. The recovery in stocks so far this year is likely to continue given easier financial conditions (i.e., lower interest rates), reasonable stock valuations, and positive—albeit slower—forecasted earnings growth. However, stocks will likely experience increased volatility later this year. While central banks remain supportive, economic growth scares and geopolitical uncertainty will continue to unnerve markets. U.S. bond returns will likely stay positive this year, with current yields around 3% for most bonds,3 combined with the Fed likely sitting tight on interest rates for a while.

Economic Review & Outlook

The U.S. economy has continued to perform well

Coming off a strong year in which growth touched near 3%,4 the U.S. economy has seen a bit of slowing in areas like housing and manufacturing, but has continued to perform well overall. The job market is still strong as business confidence remains high. Low unemployment has resulted in rising wages, which has coincided with rising consumer spending. (See Figure 2.) More recently, the U.S. economy has shown signs of improvement since the beginning of the year, as the effects of the government shutdown and heightened trade tensions appear to have worn off.

International slowdown has prompted new stimulus

Outside the U.S., economic growth across most of the major economies in the world continued to slow. Europe’s growth momentum weakened substantially, with declining manufacturing activity causing recessions in Italy, France, and Germany. At the same time, the ongoing Brexit saga has slowed the U.K. economy. In Asia, the effects of trade tensions appear to have accelerated China’s long-term secular slowdown. (See Figure 3.) The good news, however, is that China’s central bank has been more active with injecting money into its economy to maintain its growth rate above 6%. Meanwhile, central banks in Europe have responded swiftly with new stimulus measures to keep rates low to revive the continent’s struggling economies.

Global economy to continue growing, but more slowly

It is still expected that overall global economic growth, albeit lower, will likely stay positive, avoiding a global recession this year. Although the Treasury Yield Curve (often used as a recession gauge) briefly flashed a warning sign in March, the risk of a U.S. recession in 2019 is still relatively low. Growth in the U.S. will likely moderate to around 2% this year. Similarly, growth abroad will slow but remain positive as central banks mirror the Fed’s caution and continue to take careful stock of their respective economies while stimulating them when needed. As of this writing, we already see early signs of improvement in some economies.

On the Minds of Investors

Yield Curve Inversion – Is a recession forthcoming?

The U.S. Treasury Yield Curve is a line that represents interest rates (yields) of government bonds plotted against the time they have to maturity. (See Figure 4.) The curve is usually upward sloping (i.e., long-term rates are higher than short-term rates), as shown below in March 2018. The yield curve is often used as recession gauge because when it inverts (i.e., short-term rates are higher than long-term-rates), it is typically proceeded by an economic slowdown. This past March, the 3-month-to-10-year part of the curve briefly inverted.

However, the recent inversion is not such that it is signaling a severe and imminent recession. Rather, severe recessions have typically been preceded by much more significant and prolonged inversions in the 3-month-to-10-year part of the curve. Further, the more severe recessions have typically been preceded by an inversion of the entire yield curve, which we’re still far away from. Most importantly, there are many other gauges with good track records of predicting recessions, such as corporate bond interest spreads, inflation expectations, and unemployment insurance claims, that aren’t showing evidence of trouble yet. These are only some of the many market and economic indicators that we monitor very closely.

Portfolio Management

A balanced approach is warranted at this time

Although we don’t think a severe recession is imminent, we are getting further along in the economic growth cycle. As such, we have been in the process of making changes to portfolios by balancing them with longer-duration, high-grade bonds to further diversify them from stock market risk. Particularly now that we are near the end of the Fed’s latest tightening cycle, we continue to increase bond duration to better position portfolios for potential stock market declines. For similar reasons, we continue to increase bond allocations to high-quality bonds issued by governments, municipalities, and corporations, which are stable and unlikely to default.

Staying invested has worked well in 2019

Investment returns over a lifetime are largely determined by one’s behavior during the volatile times. The end of 2018 was a volatile time, and our trading activity was high with rebalancing and tax-loss-harvesting. One of our main overarching goals when trading is to keep client portfolios fully-invested by maintaining their specific allocation targets to stocks. Although this can be an emotionally difficult thing to do when stocks are falling, we make sure to help clients stick with their investment plans. So far, this disciplined approach has worked out well for portfolios in 2019 and should continue to do so in the future.

Sources

¹Morningstar Direct: U.S. stocks, as measured by Russell 3000 index, returned 16.31% in 3Q 2009.

²Morningstar Direct: The Russell 3000 index declined 20.17% from 9/21/18 to 12/25/18. The MSCI ACWI ex US IMI index declined 22.16% from 1/29/18 to 12/25/18.

³Barclays Capital: The Barclays U.S. Aggregate Bond Market Index yield is 3.0% as of 4/8/19.

⁴Bureau of Economic Analysis: U.S. economic growth was 2.9% in 2018 according to the latest estimate as of 3/28/19.

Disclosures

Please remember that different types of investments involve varying degrees of risk, including the loss of money invested. Past performance may not be indicative of future results. Therefore, it should not be assumed that future performance of any specific investment or investment strategy, including the investments or investment strategies recommended or undertaken by Capstone Financial Advisors, Inc. (“Capstone”) will be profitable. Definitions of any indices listed herein are available upon request. Please contact Capstone if there are any changes in your personal or financial situation or investment objectives for the purpose of reviewing our previous recommendations and services, or if you wish to impose, add, or modify any reasonable restrictions to our investment management services. This article is not a substitute for personalized advice from Capstone and nothing contained in this presentation is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Investment decisions should always be based on the investor’s specific financial needs, objectives, goals, time horizon, and risk tolerance. This article is current only as of the date on which it was sent. The statements and opinions expressed are, however, subject to change without notice based on market and other conditions and may differ from opinions expressed by other businesses and activities of Capstone. Descriptions of Capstone’s process and strategies are based on general practice, and we may make exceptions in specific cases. A copy of our current written disclosure statement discussing our advisory services and fees is available for your review upon request.